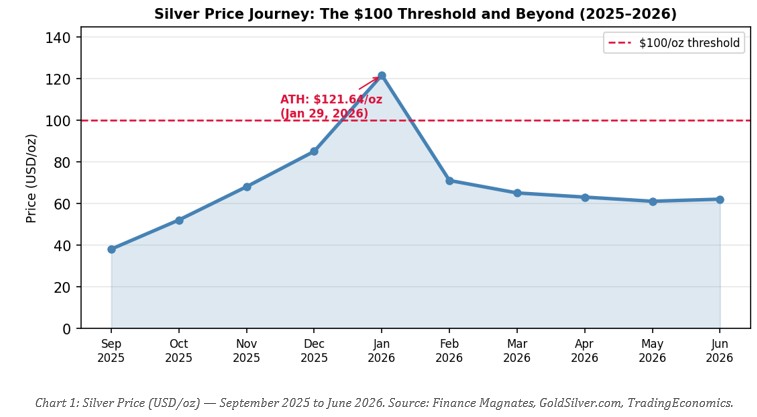

On January 29, 2026, silver crossed $121 per ounce. Not $100 — that psychological barrier was smashed weeks earlier. The metal that polite financial society calls an “industrial commodity” became, for one extraordinary moment, the most talked-about asset on the planet. Then, just as quickly, prices corrected. By late June 2026, silver was trading between $59 and $66 per ounce.

Most analysts shrugged and called it a speculative bubble. They were wrong. The spike was a fire alarm. The building has been quietly filling with smoke for years.

What happened in January 2026 was not simply about silver. It was about a system. Specifically, it was about a global financial architecture that allows paper promises to substitute for real, physical things — and what happens when people stop believing in the promises.

The Price That Shocked the System

Silver had been building momentum throughout 2025, rising approximately 144% over the year. Then came January 2026. Prices shot to a nominal all-time high of $121.64 per ounce in a single trading session. Gold simultaneously reached $5,589 per ounce. These were not arbitrary numbers produced by speculators. They were the market screaming that something fundamental was broken.

The correction that followed was equally dramatic. Silver retreated toward $71 per ounce by early February, pushed down by margin calls, a stronger dollar, and a new Federal Reserve Chair signalling tighter monetary policy. The paper market reasserted control — temporarily.

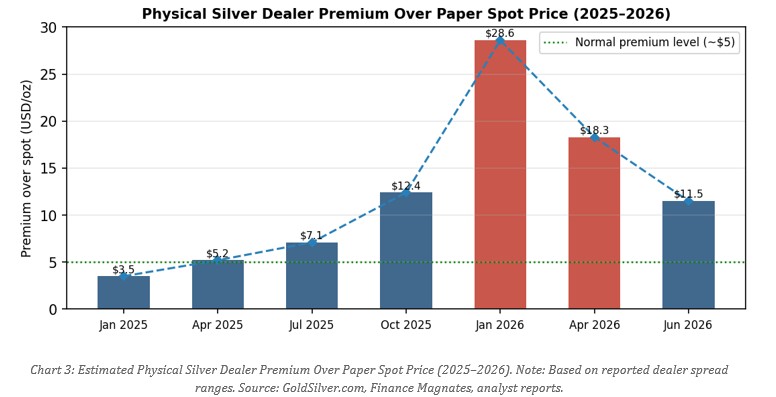

Here is where it gets interesting. The paper price recovered to the mid-60s and stabilized. But physical silver — the real metal you can hold — continued trading at premiums far above the quoted spot price. The gap between paper and physical tells you everything.

Table 1: Precious Metal Price Chronology — 2026

| Metric | Value / Date |

| Silver Intraday All-Time High | $121.64/oz — January 29, 2026 |

| Gold Intraday All-Time High | $5,589.38/oz — January 2026 |

| Silver Price (Late June 2026) | $59–$66/oz |

| Gold Price (Late June 2026) | ~$4,190/oz |

| Silver 2026 Avg Forecast (J.P. Morgan) | $81/oz |

| Silver 2026 Avg Forecast (LBMA Consensus) | $79.50/oz |

Source: Finance Magnates, GoldSilver.com, J.P. Morgan, LBMA

Table 2: Gold/Silver Ratio — Historical Comparison

| Period / Event | Gold/Silver Ratio | Interpretation |

| 2020 Pandemic Peak | 125:1 | Silver extremely cheap vs. gold |

| 1980 Bull Market Low | 17:1 | Silver historically expensive vs. gold |

| April 2025 | >100:1 | Extreme undervaluation signal |

| Mid-2026 (Stabilized) | 64–69:1 | Transitional — silver still undervalued |

| Historical “fair value” range | ~50–60:1 | Long-term average zone |

Source: GoldSilver.com, Investopedia, BullionByPost, LongtermTrends.com

Two Markets, One Metal — and a Growing Lie

To understand the silver crisis, you need to understand one concept: the difference between paper silver and physical silver.

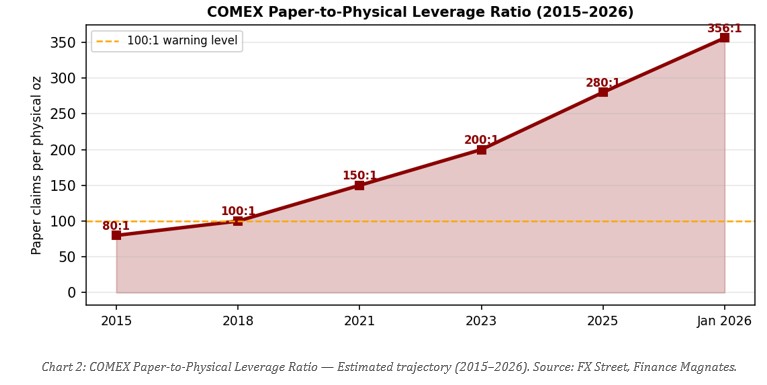

Paper silver is a financial contract — a futures contract, an ETF, a bank certificate — that promises to represent ownership of silver. Physical silver is an actual bar or coin you can touch. In theory, the paper market exists to help industry hedge risk and allow price discovery. In practice, it has grown into a vast casino where paper claims on silver vastly outnumber the actual silver that exists in vaults.

How vastly? Analysts have cited paper-to-physical leverage ratios on the COMEX exchange as high as 356-to-1. That means for every single ounce of silver available for immediate delivery, there were 356 paper claims asserting ownership of it. This works fine — until people start asking for the actual metal.

When the Vaults Started Emptying

The COMEX — the main exchange where silver futures trade in New York — categorizes its vaults in two ways. “Registered” silver is immediately available to settle a contract: you can demand delivery and it will come. “Eligible” silver meets quality standards but is not on offer for delivery yet.

The registered category is the one that matters. And it has been draining at an alarming rate. In a single week in January 2026, nearly 26% of all registered COMEX inventory disappeared. By March 2026, registered stocks fell to approximately 76 million ounces — covering only 13.4% of all outstanding contracts. Only 13.4 cents of real metal backing every dollar of paper promise. That is stress territory.

The London market told the same story. LBMA vault holdings fell from a 2020 peak of 35,667 tonnes to just 24,199 tonnes by July 2025 — a drawdown of more than 11,000 tonnes of real silver, quietly removed from the world’s largest physical settlement market.

Table 3: Exchange and Vault Inventory — Physical Silver Stress Indicators

| Metric | Figure / Date |

| COMEX Registered Inventory (March 2026) | ~76 million oz |

| COMEX Registered Inventory (June 2026) | ~87.1 million oz |

| COMEX Eligible Inventory (June 2026) | ~236.3 million oz |

| COMEX Registered Coverage of Open Interest (March 2026) | ~13.4% |

| LBMA Vault Holdings (July 2025) | 24,199 tonnes |

| LBMA Vault Holdings (May 2026) | 27,611 tonnes |

| LBMA Vault Holdings (2020 Peak) | 35,667 tonnes |

Source: LBMA, CME Group, Finance Magnates, GoldSilver.ai, Crux Investor

The Price Signals No One Was Supposed to See

Markets have a language. When physical silver becomes desperately scarce, that language gets loud.

First, the futures market flipped into backwardation. Normally, silver for delivery in the future costs more than silver today (you pay a premium for storage and time). When the market inverted — when spot silver became more expensive than futures — it was the market screaming: we need the metal NOW, not later.

Second, lease rates exploded. Lease rates are what you pay to borrow physical silver. They normally sit below 1% annually. During peak stress periods in 2025, they spiked to 35–39% per year. Think about that: to borrow silver for twelve months cost nearly 40% of its value. That is not a normal market. That is a market in crisis.

Third, delivery windows stretched from days to weeks, with some contracts settled in cash instead of metal. Cash settlement is, in practice, a form of default on the promise the paper market makes.

Why Silver? The Demand Side Has Changed Forever

Silver is not just a precious metal. It is one of the most versatile materials in modern industry. It conducts electricity better than any other substance. It kills bacteria on contact. It reflects light with extraordinary efficiency. It cannot be easily substituted in most of its applications.

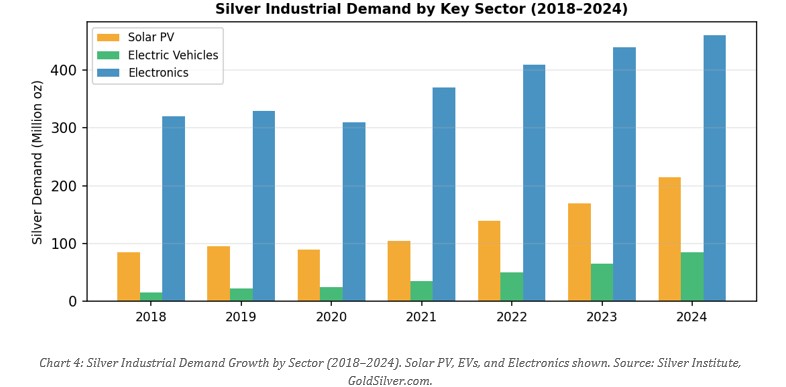

Industrial demand now accounts for over 50% of all silver consumed each year. And this demand is not optional — it is structural, driven by three of the most powerful megatrends of our era.

Solar Panels and Electric Cars: The Green Economy Runs on Silver

Every solar panel contains silver. The conductive paste that moves electricity from the panel to your grid relies on silver’s unmatched conductivity. In 2024, the solar industry consumed between 197.6 and 232 million ounces of silver — roughly 34% of all industrial consumption. As global solar capacity expands at record pace, this number only grows.

Electric vehicles add another powerful demand layer. A battery electric vehicle requires 25–50 grams of silver, roughly double the silver content of a conventional petrol car. Silver appears in power electronics, battery management systems, and the charging infrastructure that makes EVs work. With EV penetration accelerating globally, the automotive sector is on course to become the dominant silver consumer by 2027.

Artificial Intelligence and 5G: The Digital Economy’s Hidden Hunger

AI data centers consume enormous quantities of electricity. Building them requires specialized semiconductors, power delivery systems, and thermal management materials — all of which depend on silver. The irony is elegant: the AI revolution’s enormous energy needs are driving massive solar build-out, which in turn creates even more silver demand.

5G network base stations require three to five times more silver than the 4G equipment they replace. Each new tower adds to a global demand curve that runs relentlessly upward.

Table 4: Silver Industrial Demand by Key Sector — 2024

| Sector | Estimated Consumption (2024) |

| Total Industrial Demand | 680.5 million oz (Record High) |

| Electronics and Semiconductors | ~460.5 million oz |

| Solar Photovoltaics (PV) | ~197.6–232 million oz |

| Chemical Catalysts (Ethylene Oxide) | ~42 million oz |

| Medical Applications | ~28 million oz |

Source: Silver Institute World Silver Survey 2025, GoldSilver.com

The Supply Side Cannot Keep Up

2026 marks the sixth consecutive year in which the silver market has consumed more than it has produced. The official deficit projected by the Silver Institute for 2026 is 46.3 million ounces. Since 2021, this ongoing shortfall has drained a cumulative 762 million ounces from global above-ground stockpiles.

Why can’t production simply catch up? Because silver has a geological problem: 70–80% of all mined silver comes out of the ground as a byproduct of mining other metals — copper, lead, zinc, gold. Mining companies make their investment decisions based on those primary metals, not silver. A surge in the silver price does not automatically trigger a surge in silver mining.

Even when a company decides to open a dedicated silver mine, it takes 7 to 15 years from discovery to first production. The world’s major silver mines are maturing, with declining ore grades. Global production actually fell — from 26,000 metric tons in 2023 to 25,000 metric tons in 2024. A projected 1% rise in 2026 to 820 million ounces barely makes a dent in the deficit.

Table 5: Top Silver-Producing Countries — 2024 Estimates

| Country | Production (Metric Tons, 2024 Est.) |

| Mexico | 6,300 |

| China | 3,300 |

| Peru | 3,100 |

| Bolivia | 1,300 |

| Poland | 1,300 |

| Chile | 1,200 |

| Russia | 1,200 |

| World Total | 25,000 |

Source: U.S. Geological Survey (USGS) Mineral Commodity Summaries 2025

China’s Export Controls: The Shock That Fragmented the Market

On January 1, 2026, China — one of the world’s dominant silver refiners — officially reclassified silver as a strategic material and imposed strict export controls. This single policy decision effectively split the global silver market into regional islands: Asia, Europe, and North America, no longer freely exchanging metal.

The physical arbitrage trade that normally keeps prices aligned across continents was crippled overnight. Silver in Shanghai began trading at persistent premiums to the paper prices in London and New York. Real metal was being pulled eastward, away from the very exchanges that the world uses to “discover” the silver price. A market where the price is set in places that are running out of metal is a market with a credibility problem.

Silver’s Return to Money — and What It Tells Us About the Dollar

For thousands of years, silver was money. Not a representation of money, not a promise of money — actual money. That role was progressively stripped away through the 20th century, culminating in the final severance of the dollar from gold in 1971. Since then, the global monetary system has operated on pure faith in government-issued paper currencies.

That faith is fraying. And silver is beginning, quietly, to return.

Central Banks Are Buying Silver Again

Russia has been allocating sovereign funds to acquire precious metals including silver as part of an explicit de-dollarization strategy. The Reserve Bank of India has made silver eligible for loan collateral — integrating it formally into the banking system. Saudi Arabia has gained exposure to silver through exchange-traded products. These are not fringe moves by small economies. These are sovereign decisions by major global players.

Meanwhile, BRICS+ nations have collectively accumulated over 6,000 metric tons of gold reserves as they work to reduce reliance on the U.S. dollar. Silver is increasingly seen as a “higher-beta” complement — cheaper to accumulate, with dual value as both industrial input and monetary reserve. Even modest central bank allocations to silver would place overwhelming demand pressure on an already-deficient market.

The Petrodollar System and the Architecture of Modern Money

The dollar’s global dominance rests on two pillars: its role as the world’s reserve currency, and the petrodollar system — the arrangement by which global oil trade is priced and settled in dollars. This forces every country that imports energy (which is almost everyone) to hold dollars, creating artificial, sustained global demand for the currency.

This system is under unprecedented stress. The geopolitical realignment underway — Russia, China, and the BRICS bloc actively constructing alternative trade and settlement frameworks — is not a temporary political disagreement. It is a structural challenge to the architecture of global finance. When countries stop needing dollars to buy oil, the demand for dollars falls. When the demand for dollars falls, the purchasing power of dollar savings erodes.

In that environment, assets with finite supply and intrinsic utility — like silver — become enormously attractive. Silver cannot be printed. It cannot be debased by a central bank decision. Its industrial demand creates a permanent consumption floor. Its historical role as money gives it credibility as a store of value. The combination is rare.

The Paper Market’s Dirty History

The fractional reserve structure of the paper silver market is not a neutral fact of financial life. It has a history. In September 2020, JPMorgan Chase paid a record $920 million settlement for a multi-year “spoofing” scheme in gold and silver futures that ran from 2008 to 2016. Multiple traders were subsequently sentenced to prison. Other major banks collectively paid over a billion dollars more in similar penalties.

Spoofing means placing large orders with no intention of executing them, purely to move the price in a desired direction, then cancelling those orders and trading in the opposite direction. This was done routinely, systematically, for nearly a decade, in the market that is supposed to set the “real” price of silver.

As of mid-2026, regulators have not issued new findings related to the 2024–2026 market activity. The CFTC maintains that concentrated short positions often reflect legitimate hedging. But the structural fragility remains. When the market’s foundational assumptions are challenged — as they were in early 2026 — the memory of past manipulation makes trust nearly impossible to rebuild overnight.

What This All Means: Follow the Metal, Not the Narrative

Step back and look at the full picture. You have an industrial demand profile that is growing relentlessly, driven by technologies the world has decided it cannot live without. You have a supply side that is structurally unable to respond to price signals. You have six consecutive years of deficits draining global inventories. You have exchange vaults emptying. You have paper claims that outnumber real metal by hundreds to one.

And you have a global monetary system in the early stages of a historic realignment — away from dollar dominance and toward a more multipolar structure where tangible assets matter more than ever.

The silver surge of 2026 did not come from nowhere. It was the inevitable result of years of pressure building inside a system designed to substitute promises for reality. The correction that followed did not resolve the underlying problem. The inventory is still depleted. The deficit continues. The de-dollarization trend is still unfolding. The industrial demand megatrends are not reversing.

The paper price may say one thing. The physical market whispers another. History suggests that when the two diverge far enough, for long enough, it is the paper that ultimately yields — not the metal.

The great disconnect is not closing. It is widening.

Glossary

All-Time High (ATH): The highest price a financial asset has ever reached. Silver’s ATH as of January 2026 was $121.64 per ounce.

Backwardation: Normally, silver for delivery next month costs a bit more than silver today (because of storage costs). Backwardation is when this flips — silver today costs MORE than silver later. It means the market is desperate for physical metal RIGHT NOW, not in the future.

BRICS+: A group of major emerging-market nations: Brazil, Russia, India, China, South Africa, and several newer members. They are working together to reduce their dependence on the U.S. dollar in international trade.

Bullion Bank: A large bank that specialises in trading gold, silver, and other precious metals — both the physical metal and financial contracts based on it.

Byproduct Mining: When a mining company primarily extracts one metal (like copper or zinc) and silver comes out of the ground as a side product. Because the company’s decisions are based on the primary metal’s price, silver production does not automatically increase just because silver’s price rises.

CFTC (Commodity Futures Trading Commission): The U.S. government agency responsible for overseeing the futures and derivatives markets. They watch for illegal manipulation and set rules for exchanges like the COMEX.

COMEX: Short for Commodity Exchange. It is the main market in New York where silver and gold futures contracts are traded. Think of it as the world’s biggest betting shop for metal prices — but with real metal supposedly sitting in vaults behind it.

Contango: The normal state of a futures market: silver for future delivery costs more than silver today. When this structure reverses, you have backwardation (see above).

De-dollarization: The global trend of countries reducing their use of the U.S. dollar in international trade and reserves. Countries increasingly want to trade and save in other currencies, commodities, or assets to reduce their exposure to U.S. financial policy.

Deficit (Market): When the world consumes more silver in a year than it produces. The difference must come from existing stockpiles. Six consecutive years of this has significantly depleted global silver reserves.

Eligible Inventory: Silver sitting in a COMEX vault that meets exchange quality standards but is NOT available for immediate contract settlement. Think of it as silver in a holding room, not yet on the market.

Fiat Currency: Money that has value because a government says it does — not because it is backed by a physical commodity like gold or silver. The U.S. dollar, the Euro, and virtually every other modern currency is fiat money.

Fractional Reserve System: A system where a small amount of real assets backs a much larger number of claims on those assets. In banking, a bank keeps only a fraction of deposits as actual cash. In the silver market, a small amount of physical silver backs a very large number of paper contracts.

Futures Contract: A financial agreement to buy or sell a specific amount of silver at a fixed price on a specific future date. Most futures contracts are never actually settled with real metal — they are traded and closed out before delivery is due.

Gold/Silver Ratio: How many ounces of silver it takes to buy one ounce of gold. If gold is $4,000 and silver is $64, the ratio is 62.5:1. Historically, a ratio above 80:1 has often meant silver is cheap relative to gold.

Hedge / Hedging: A financial strategy used to reduce risk. A silver miner might sell futures contracts to lock in today’s price so they are protected if prices fall before they dig the silver out. Legitimate hedging is legal; using it to manipulate prices is not.

Intraday High: The highest price reached during a single trading day — even if the day closed lower. Silver’s intraday high of $121.64 on January 29, 2026 is its all-time nominal record.

Lease Rate: The interest rate charged to borrow physical silver. Normally below 1% per year. When lease rates spiked to 35–39% during the 2025 crisis, it meant physical metal was almost impossible to find in the wholesale market.

LBMA (London Bullion Market Association): The trade association that oversees the global over-the-counter precious metals market based in London. Its member banks are where most of the world’s wholesale gold and silver trade happens outside of exchanges like COMEX.

Leverage (Financial): Using borrowed money or financial instruments to control a much larger position than your own capital would allow. 356-to-1 leverage in the paper silver market means one ounce of real silver supports 356 ounces of paper claims.

Nominal Price: A price expressed in today’s dollars without adjusting for inflation. Silver’s “nominal” all-time high was $121.64. Its “real” (inflation-adjusted) high was in January 1980 when it briefly touched $50 — equivalent to several hundred dollars in 2026 money.

Open Interest: The total number of outstanding futures contracts that have not yet been settled or closed. High open interest relative to available physical inventory is a stress signal.

Paper Silver: Any financial instrument that claims to represent silver ownership without you physically holding the metal. This includes futures contracts, exchange-traded funds (ETFs), and bank certificates.

Petrodollar System: The arrangement, established in the 1970s, where global oil trade is priced and settled in U.S. dollars. This creates permanent global demand for dollars because any country that imports oil needs dollars to pay for it. The system is being gradually challenged by major oil-exporting and oil-importing nations.

Physical Silver: Actual silver metal — bars, coins, or granules — that you can touch. Opposed to paper silver, which is just a promise.

Registered Inventory: Silver in a COMEX vault that has been “registered” with an official warrant and is immediately available to settle a futures contract. This is the critical pool of real metal that actually backs the paper market.

Solar PV (Photovoltaics): The technology that converts sunlight directly into electricity. Silver is used in the conductive paste inside solar cells because it conducts electricity better than almost anything else.

Spoofing: An illegal trading practice where a trader places large buy or sell orders with no intention of executing them, purely to make other traders think the market is moving in a particular direction. Once others react, the spoofer cancels the fake orders and trades in the opposite direction for profit. JPMorgan paid $920 million to settle spoofing allegations in 2020.

Strategic Reserve Asset: An asset held by a government or central bank as a store of value and financial security. Gold has traditionally been the main strategic reserve metal; some sovereign entities are now considering silver in this role.

Structural Deficit: A supply-demand gap that is not caused by a temporary event but by deep, lasting structural factors. Silver’s six-year consecutive deficit is structural because industrial demand growth fundamentally outpaces mining supply growth.

Thrifting: In manufacturing, the process of engineering products to use less of an expensive input material. Solar panel makers have worked to reduce silver content per cell, but the sheer volume of panels being deployed has overwhelmed these efficiency gains.

Sources and References

[1] GoldSilver.com — Silver Price Outlook June 2026. https://goldsilver.com/industry-news/article/silver-price-outlook-june-2026/

[2] GoldSilver.com — Silver Price Forecast 2026–2027. https://goldsilver.com/industry-news/article/silver-price-forecast-2026-2027-the-bull-case-and-bear-case-laid-out/

[3] GoldSilver.com — Silver Price Forecast Predictions. https://goldsilver.com/industry-news/article/silver-price-forecast-predictions/

[5] USA Gold — Daily Silver Price History. https://www.usagold.com/daily-silver-price-history/

[6] Finance Magnates — COMEX Inventory Tightens, New Silver Price Predictions. https://www.financemagnates.com/trending/how-high-can-silver-go-in-2026-as-comex-inventory-tightens-new-silver-price-predictions-from-bofa-citi-and-reuters-target-300/

[7] Investing News Network — Highest Silver Price Records. https://investingnews.com/daily/resource-investing/precious-metals-investing/silver-investing/what-was-the-highest-price-for-silver/

[9] Investopedia — Historical Guide to Gold/Silver Ratio. https://www.investopedia.com/articles/investing/080316/historical-guide-goldsilver-ratio.asp

[12] LongtermTrends.com — Gold/Silver Ratio. https://www.longtermtrends.com/gold-silver-ratio/

[14] MetalCharts.org — COMEX Inventory. https://metalcharts.org/comex/inventory

[15] GoldSilver.com — Gold Price Forecast 2026–2027. https://goldsilver.com/industry-news/article/gold-price-forecast-2026-2027-key-predictions-from-top-analysts/

[17] Investing.com — Silver Flashes Rare Warning Signal as Physical Market Seizes Up. https://www.investing.com/analysis/silver-flashes-rare-warning-signal-as-physical-market-seizes-up–bofa-targets-65-200668602

[18] TradingKey — 2026 Silver Physical Squeeze. https://www.tradingkey.com/analysis/commodities/metal/261487879-2026-silver-physical-squeeze-strategic-asset-tradingkey

[19] GoldSilver.ai — COMEX Silver Inventory. https://goldsilver.ai/metal-prices/comex-silver

[20] Crux Investor — Best Silver Stocks 2025, Deficit Market. https://www.cruxinvestor.com/posts/best-silver-stocks-2025-deficit-market-creates-gains

[21] FX Street — Physical Silver Demand Challenging Paper Futures Market. https://www.fxstreet.com/analysis/physical-silver-demand-is-challenging-paper-driven-futures-market-202602171934

[23] Yahoo Finance — Silver Market Forecast Trends Outlook. https://finance.yahoo.com/news/silver-market-forecast-trends-outlook-112700359.html

[24] Silver Institute — Silver Demand Forecast Across Key Technology Sectors. https://silverinstitute.org/silver-demand-forecast-to-expand-across-key-technology-sectors/

[25] LBMA — London Vault Data. https://www.lbma.org.uk/prices-and-data/london-vault-data

[27] GoldSilver.com — Silver Industrial Demand: Solar, EVs, and the Supply Gap. https://goldsilver.com/industry-news/article/silver-industrial-demand-solar-evs-and-the-supply-gap/

[29] Grokipedia — World Silver Survey 2025. https://grokipedia.com/page/World_Silver_Survey_2025

[30] Silver Institute — Silver Industrial Demand Record 680.5 Moz in 2024. https://silverinstitute.org/silver-industrial-demand-reached-a-record-680-5-moz-in-2024/

[31] USGS — Mineral Commodity Summaries 2025 (Silver). https://pubs.usgs.gov/periodicals/mcs2024/mcs2024-silver.pdf

[35] GoldSilver.com — Silver Market Deficit 2026: Six Years and Getting Worse. https://goldsilver.com/industry-news/goldsilver-news/silver-market-deficit-2026-six-years-and-getting-worse/

[36] Silver Institute — Global Silver Investment to Remain Strong in 2026. https://silverinstitute.org/global-silver-investment-to-remain-strong-in-2026-against-the-backdrop-of-a-sixth-consecutive-annual-market-deficit/

[37] Gainesville Coins — Central Bank Silver Purchases: Russia Smart Money 2025. https://www.gainesvillecoins.com/blog/central-bank-silver-purchases-russia-smart-money-2025

[38] Discovery Alert — Central Banks Silver Buying Trend 2025. https://discoveryalert.com.au/central-banks-silver-buying-trend-2025/

[39] GoldSilver.com — Silver’s Big Comeback: 3 Central Banks Already In. https://goldsilver.com/industry-news/video/silvers-big-comeback-3-central-banks-already-in-whats-next/

[43] Factually.co — Evidence on CFTC/DOJ Misconduct Linked to Silver Since 2024. https://factually.co/fact-checks/finance/evidence-regulators-cftc-doj-cme-bank-misconduct-linked-to-silver-since-2024-5deb67

[44] Navnoor Bawa Substack — Eight Banks Paid $13B for Silver Manipulation. https://navnoorbawa.substack.com/p/eight-banks-paid-13b-for-silver-manipulation

[45] CFTC Press Release 8260-20 — JPMorgan $920M Settlement. https://www.cftc.gov/PressRoom/PressReleases/8260-20