The Federal Reserve, the Fed, started overnight reverse repo transactions in 2013. The aim of reverse repo transactions is to control the short-term interest rates. Reverse repo (RRP), reverse repurchase agreements, is a transaction that central banks implement when they want to reduce excess cash in the market. In this way, it is aimed to suppress the downward interest rate. The central bank takes money from banks and issues bonds in return.

This pressures interest rates below the market level. Repo deals are only with primary dealers, while reverse repo agreements are executed with both primary dealers and extended reverse repo counterparties, which include banks, government-backed businesses, and money market funds (https://www.newyorkfed.org/markets/domestic-market-operations/monetary-policy-implementation/repo-reverse-repo-agreements).

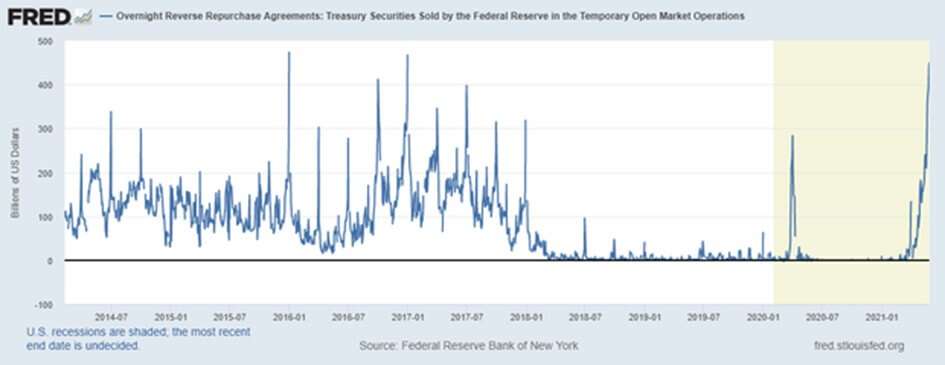

Towards the end of May, the FED made a large-volume reverse repo transaction. This is recorded as the highest level. Approximately $485 billion. We can say that reverse repo transactions have increased since March (https://www.reuters.com/article/usa-fed-reverse-repo-idUSL2N2NE2FH).

Figure 1. FED Reverse Repo

Source: fred.stlouisfed.org

As can be seen in the chart, the last volume of transactions close to this huge reverse repo transaction made by the Fed was between January 2016 and January 2017. This reverse repo transaction made by the FED is perceived as withdrawing from the market as a result of the excess money being printed. However, it is useful to interpret it as follows: banks buy short-term bonds, that is, 1-month and 3-month bonds, which increases the interest rates of these bonds.

In fact, we can understand from here that there is a problem in the system. That is, large banks are protected and their balance sheets are audited, but this is not the case for small banks and bank-like institutions (shadow banks). Since they give leveraged loans, they have to guarantee their short-term cash conditions.

In other words, there is no question of the FED printing too much money and flooding the market with money. As can be seen in Figure 2, while bond purchases under 1 month increase the interest rates, long-term bonds have low rates together with the sales. This creates the perception that there is a trust problem in the system.

In addition, considering the expenditures that the FED is making, there is a thought that it will borrow more and interest rates will increase in the long run. If the FED chooses to raise interest rates or collect cash from the market, thinking that there is enough cash in the market from these short-term bond purchases by banks, this time, the repo shocks experienced in 2018 and 2019 may repeat and it may have to print even more money.

Figure 2. FED Treasury Bond Rates

Source: https://www.cnbc.com/us-treasurys/