![]()

Yuan, war, energy, and the quiet attempt to redesign the financial map

There are moments in history when the surface looks calm, but under that calm, something important is moving. The financial system is often like that. On the outside, the dollar still looks untouchable. It is still the main reserve currency. It is still the deepest market. It is still the language of global finance. But under that surface, another process is growing, patient and strategic. China is not trying to replace the dollar in one dramatic night. China is trying to build a world where the dollar is no longer the only door.

This is why the rise of the yuan should not be read as a simple currency story. It is a power story. It is about trade routes, payment systems, sanctions, oil flows, technology, and political pressure. A currency becomes global not only because it is strong, but because it can travel. It needs roads, ports, pipes, banks, contracts, trust, and also fear. Sometimes a currency rises because people love it. Sometimes it rises because people need an escape route from something else.

Today, China is building that escape route. Slowly. Quietly. Step by step.

The real question is not whether the yuan has already defeated the dollar. It has not. The real question is whether China is preparing the architecture of the next financial era while much of the world is still watching only the old one.

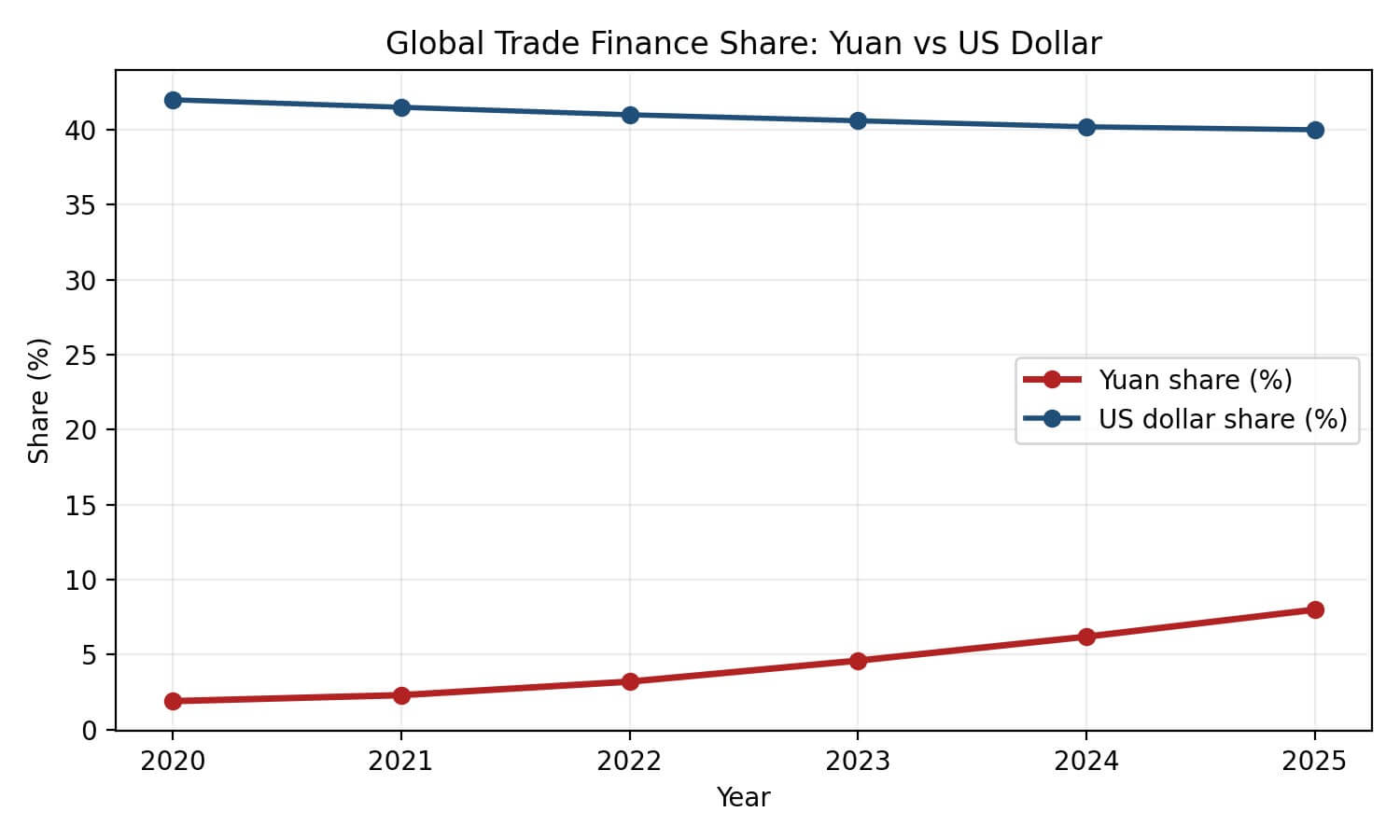

The factual picture is now clearer than many people admit. In trade finance, the yuan has moved far beyond symbolism. Reporting based on SWIFT data indicates that its share rose from just under 2% in 2020 to about 8% by early 2025. That is still far below the dollar, but it is not small when we think in structural terms. It shows movement. It shows direction. It shows that some part of the world is already changing its habits.

Figure 1. Global trade finance share: yuan vs US dollar (illustrative compilation based on SWIFT-linked reporting and public commentary).

| Year | Yuan share (%) | US dollar share (%) |

| 2020 | 1.9 | 42.0 |

| 2021 | 2.3 | 41.5 |

| 2022 | 3.2 | 41.0 |

| 2023 | 4.6 | 40.6 |

| 2024 | 6.2 | 40.2 |

| 2025 | 8.0 | 40.0 |

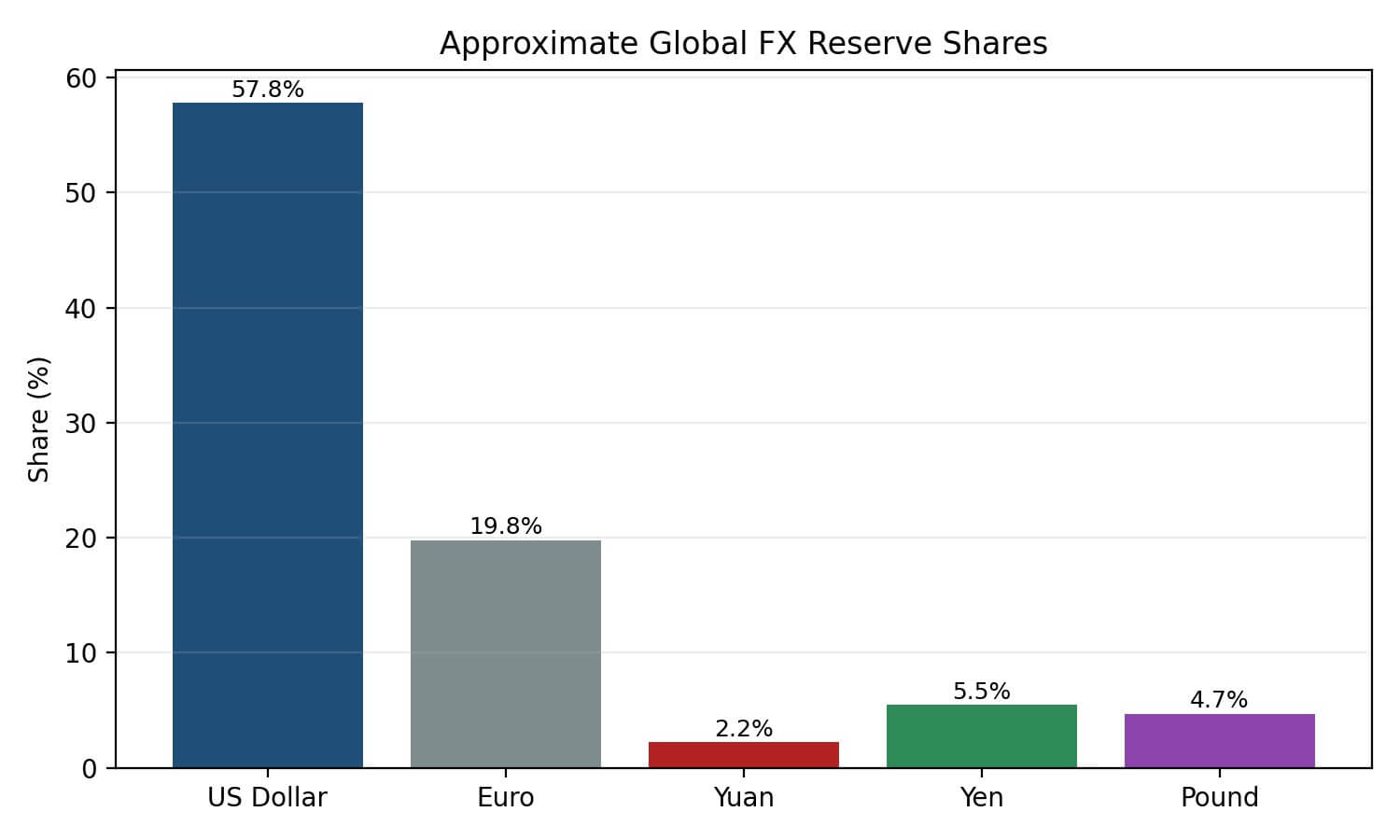

But reserve currency status tells a different story. According to IMF COFER data, the yuan still accounts for only a small share of official foreign exchange reserves. The dollar remains far ahead. The euro also remains much larger. This means the yuan is growing first where necessity is strong, not where trust is already complete. It is growing in settlement, in bilateral use, in sanctions-sensitive corridors, and in strategic trade. It is becoming a tool of use before becoming a tool of deep confidence.

That difference matters because international monetary power has layers. One layer is payment. Another is invoicing. Another is reserve management. Another is legal confidence. Another is geopolitical backing. China is not yet dominant in all these layers. But it does not need to be dominant in all of them to matter. It only needs to become necessary in enough of them.

Figure 2. Approximate global FX reserve shares. The yuan is visible, but still small compared with the dollar and euro.

| Currency | Approximate share (%) |

| US Dollar | 57.8 |

| Euro | 19.8 |

| Yuan | 2.2 |

| Yen | 5.5 |

| Pound | 4.7 |

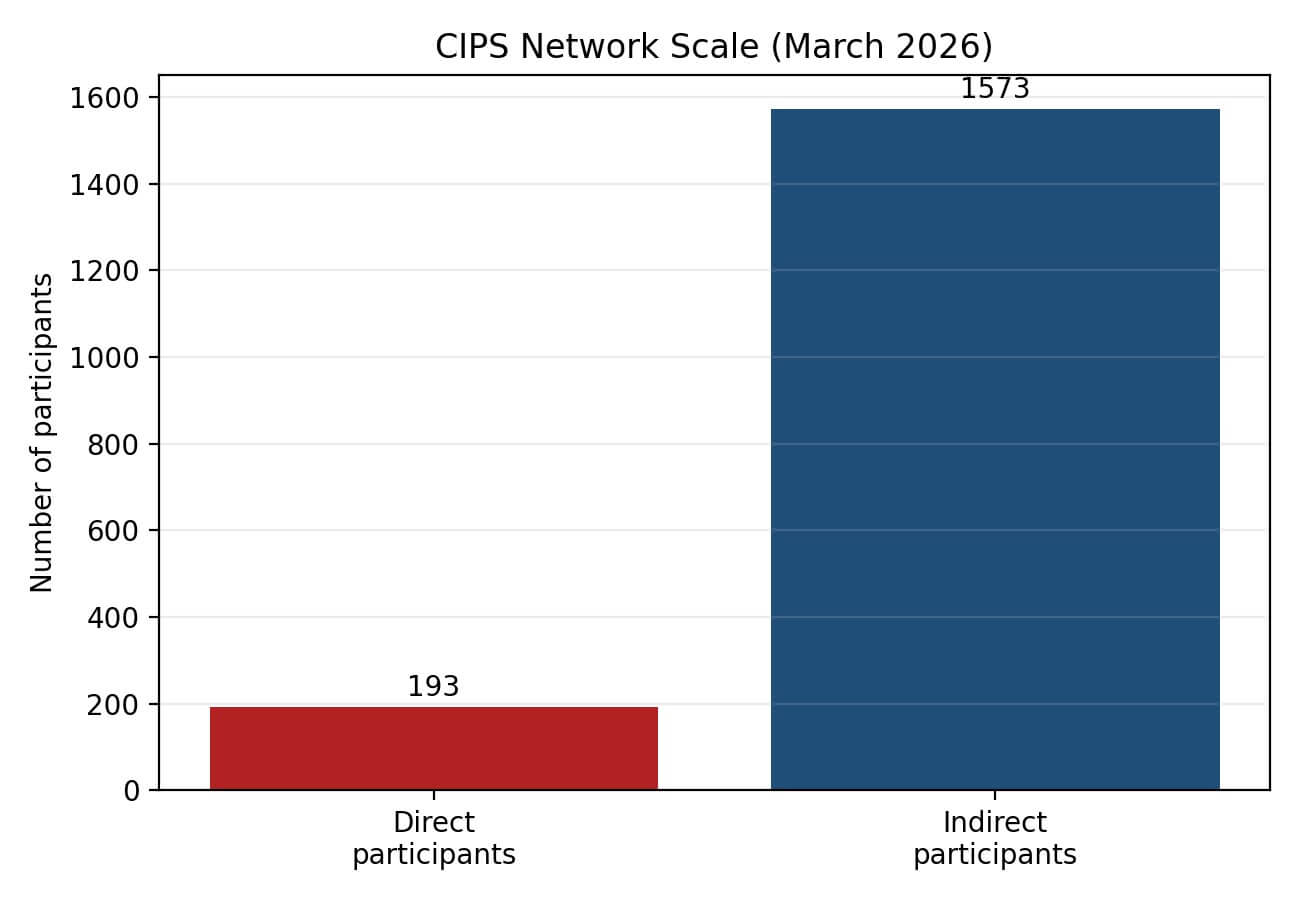

This is why CIPS matters. Many people look at payment infrastructure as if it were just plumbing. It is not. It is power with wires and rules. Once a country can settle more transactions outside the old channels, it gains strategic breathing space. CIPS is still much smaller than the full Western financial architecture, but it is growing, and growth is the point. Beijing is building institutional muscle before the real stress test arrives.

Figure 3. CIPS network scale in March 2026. Size matters because payment networks create strategic resilience.

| CIPS participation type | Count |

| Direct participants | 193 |

| Indirect participants | 1573 |

Energy is the second layer. Oil is not only about fuel. Oil is about the map of influence. For decades, the petrodollar system gave deep support to the dollar order. If even a part of energy trade moves into yuan settlement, the meaning is bigger than one invoice. It means financial habit starts to shift. And habits, once repeated enough, become structure.

This is where the Iran-United States-Israel war enters the story. A war in that region is not only a military event. It is a pricing event. It changes freight, insurance, risk, shipping expectations, and the cost of strategic dependence. The Strait of Hormuz is one of the narrowest points on the map, but it sends some of the widest financial signals in the world. If that corridor becomes unstable, then the countries most exposed to imported energy begin to think differently.

China thinks in terms of exposure. The lesson for Beijing is simple: if your rival can use the dominant financial system as a weapon, then you must reduce the number of places where you can be cornered. This is why sanctions matter so much in the story of the yuan. The freezing of reserves, the blocking of channels, and the use of payment systems as pressure points did not only punish specific states. They educated the rest of the world. They taught others what dependence can cost.

Iran has become especially important in this environment. It is not because Iran is stable. It is because Iran is constrained. Once a country is pushed outside the smooth functioning of the dollar system, alternative channels become more valuable. China can learn from every such corridor. It can observe what works, what fails, what holds under pressure, and what kind of partners accept non-dollar mechanisms when necessity is high enough.

India does not want to live inside a Chinese financial order, but India also does not want to be trapped. If Middle East risk rises and supply lines become more fragile, India may behave with even more commercial pragmatism. The same is true in a different form for Japan. Japan is much closer to the American strategic system, but energy pressure has its own logic. Countries speak one language in diplomacy and another in procurement.

For this reason, the future may not be a clean transfer from dollar to yuan. The more realistic future is fragmentation. The dollar remains the main reserve anchor. The yuan expands where strategic need is highest. Regional settlement becomes more common. Central banks stay cautious. Payment systems diversify. The world becomes less unified and more layered.

This is where I think China’s real strategy becomes visible. China may not be trying to win with one dramatic blow. It may be trying to become impossible to isolate. Build the payment rails. Build the trade links. Build the commodity channels. Build the bilateral habits. Build the alternatives before the next major global stress event. This is not theater. This is patient statecraft.

The pandemic question should be handled carefully. There is a factual part and a speculative part. The factual part is that the WHO has worked on a pandemic agreement framework and governments have debated future preparedness. The speculative part is the stronger claim that a new pandemic is being deliberately prepared to create cover for a financial reset centered on China. At this stage, public evidence does not prove that stronger claim. And if we care about serious analysis, we must say that plainly.

Still, serious caution does not mean blindness. Crises do accelerate structural change. Wars reshape energy routes. Financial panics reshape regulation. Pandemics reshape public finance, digital systems, emergency governance, and supply chains. So while we cannot claim proof of a deliberate China-origin pandemic plan for yuan expansion, we can say something else with confidence: if a major global shock happens, China is better positioned than before to use that moment in support of its long monetary strategy.

This is why the yuan story is not only about numbers. It is about timing, infrastructure, and strategic patience. The currency does not need to replace the dollar tomorrow. It only needs to become normal in more places. That is how systems change. Not always with a crash. Sometimes with a quiet rerouting.

So what is China trying to do? In my reading, China is trying to create a world in which the use of the dollar is no longer automatic. A world in which more countries keep an alternative lane open. A world in which pressure from Washington loses some force because financial traffic can move another way. This is not yet the end of the dollar world. But it may be the early construction phase of a more divided one.

And that may be the most important truth of all. The next monetary order may not arrive as a single new empire. It may arrive as a map of competing channels. In that map, the yuan does not need to rule everything. It only needs to become too relevant to ignore.

Arzu ALVAN

March 2026

Sources used for factual grounding

- IMF COFER: https://data.imf.org/COFER

- SWIFT Global Currency Tracker: https://www.swift.com/our-solutions/compliance-and-shared-services/business-intelligence/renminbi/rmb-tracker

- CIPS: https://www.cips.com.cn/en/index/index.html

- BIS Triennial Survey: https://www.bis.org/statistics/rpfx22.htm

- WHO pandemic agreement news: https://www.who.int/news/item/16-04-2025-who-member-states-conclude-negotiations-and-make-significant-progress-on-draft-pandemic-agreement

- IntelliNews on yuan trade finance: https://www.intellinews.com/yuan-s-share-in-global-trade-finance-quadruples-to-8-as-de-dollarisation-continues-424729

- Nikkei Asia on India: https://asia.nikkei.com/spotlight/iran-tensions/Iran-war-upends-India-s-pivot-from-Russian-oil

- Nikkei Asia on Japan: https://asia.nikkei.com/spotlight/iran-tensions/Iran-attacks-leave-Japan-balancing-US-ties-and-energy-security