Seventy-three percent. Hold that number in your mind for a moment. Not a majority of disgruntled economists. Not a fringe of conspiracy theorists. We are talking about 73 of the world’s own central banks — the very institutions that guard their nations’ sovereign wealth, that sit at the apex of global finance, that have spent decades building their reserves in U.S. dollars — and in 2025, nearly three-quarters of them told the World Gold Council the same thing: they expect the dollar’s share of global reserves to fall. Significantly. In the next five years.

That is not a market signal. That is not a passing sentiment. It is a verdict. And when the judges are the world’s monetary authorities, every investor, every policymaker, and honestly every thinking person on the planet should pay attention.

So what is happening? Why are the guardians of the world’s reserve system quietly stepping away from the asset that once underpinned it? And what are they buying instead? The answers tell a story about trust, power, and the way money itself is being reinvented.

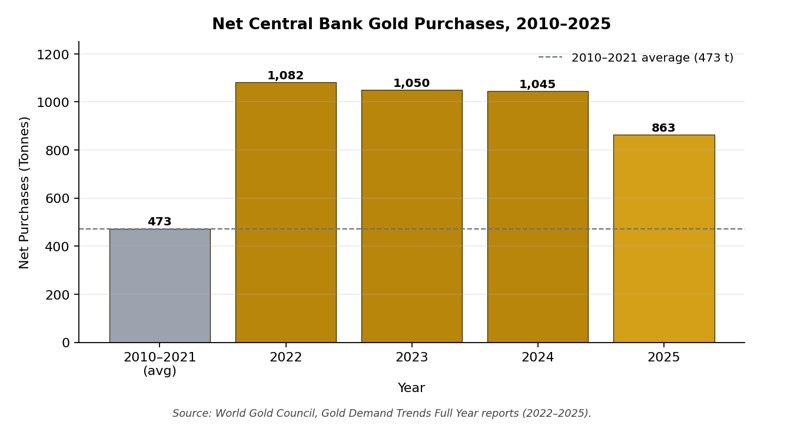

863 Tonnes. Every Single Year. This Is No Accident.

In 2025, the world’s central banks collectively purchased 863 tonnes of gold. This is confirmed by the World Gold Council’s official data. The number sounds dry until you consider the context: in the decade before 2022, the average annual purchase was around 473 tonnes. Then, starting in 2022, something broke open. Central banks bought over 1,000 tonnes per year, for three consecutive years, shattering every modern record. Even in 2025, when some slowing was expected, the total landed at nearly double the pre-2022 baseline.

Think of it this way. Imagine a family that used to spend €500 a month on groceries. Then something changed at the supermarket — maybe the quality collapsed, maybe the owner started threatening customers — and suddenly they started spending €1,100 a month. A year later, they spend €900. Some analysts say: ‘Look, they’re cutting back.’ But the truth is they are still spending nearly twice what they used to. The new normal is not the old normal. The behavior has permanently changed.

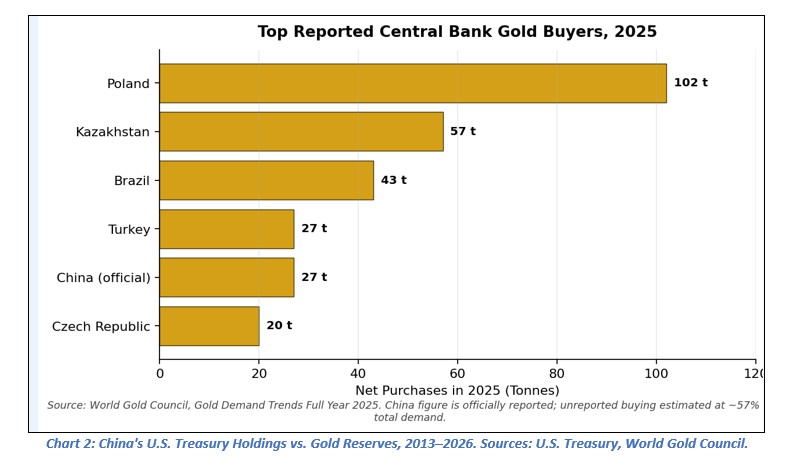

The buyers in 2025 were geographically wide. Poland’s central bank led the field with 102 tonnes — its second consecutive year at the top. Kazakhstan added 57 tonnes, its highest annual purchase since 1993. Brazil re-entered the market after four years away, picking up 43 tonnes. Turkey added 27 tonnes, as did China officially. The Czech Republic quietly added 20 tonnes as part of a steady, multi-year program.

There is also a hidden layer to this story. The World Gold Council estimates that roughly 57% of total central bank demand in 2025 came from buyers who never publicly reported their purchases. These are institutions — widely suspected to include China and others — who accumulate gold through state-owned enterprises or commercial banks to avoid moving the price against their own future purchases. When you account for this unreported buying, some independent estimates put the true 2025 figure closer to 1,237 tonnes. The disclosed number is already striking. The full picture may be even more so.

Table 1: Major Central Bank Gold Purchases, 2025

| Country / Institution | Reported Purchase (Tonnes) | Key Driver | Source |

| National Bank of Poland | 102 | National financial security; second consecutive year as top buyer | WGC 2025 |

| National Bank of Kazakhstan | 57 | Record purchase since 1993; leverages domestic mine output | WGC 2025 |

| Central Bank of Brazil | 43 | Re-entered market after four-year absence (Q3/Q4 purchases) | WGC 2025 |

| Central Bank of Turkey | 27 | Consistent multi-year accumulation program | WGC 2025 |

| People’s Bank of China | 27 | Official reported figure; widely believed to hold additional unreported positions | WGC 2025 |

| Czech National Bank | 20 | Steady ongoing program to increase gold share of reserves | WGC 2025 |

| Total (All Reported) | 863.3 | Net central bank purchases globally, 2025 | WGC 2025 |

Source: World Gold Council, Gold Demand Trends Full Year 2025. Unreported buying estimated at ~57% of total demand.

|

Chart 1: Net Central Bank Gold Purchases, 2010–2025 (Tonnes). Source: World Gold Council.

The Survey That Changed Everything

Each year, the World Gold Council conducts a survey of the world’s reserve managers. These are the professionals who sit inside central banks and decide how to protect their nation’s wealth. In 2025, a record 73 central banks responded — the highest participation in the survey’s history. What they said was remarkable.

Seventy-three percent of respondents expect the U.S. dollar’s share of global reserves to be lower — moderately or significantly — within five years. Read that sentence again. These are not academics speculating in journals. These are the people who actually manage the world’s reserve assets, day by day, making real decisions that determine what their nations’ wealth looks like a decade from now.

And it is not merely an opinion. Opinion translates into action. A record 43% of those same central banks told the survey they plan to increase their gold holdings in the coming twelve months. Zero said they planned to decrease them. Ninety-five percent expect total global official gold reserves to rise over the next year. These are not passive observers of a trend. They are the trend.

By 2026, the data had grown even more assertive. A follow-up survey — this time with 76 central bank respondents — found 45% planning to add gold, another record. Eighty-three percent said they expect gold’s share of total reserves to be higher in five years. The motivations they cited were consistent and telling: crisis protection (90% of respondents), long-term store of value (84%), and portfolio diversification (82%).

The language of ‘crisis protection’ and ‘store of value’ matters here. These are not reasons to hold an asset when everything is fine. They are reasons to hold an asset when you are not sure everything will remain fine. Read between the lines: the world’s reserve managers are buying insurance. Insurance against what? That is the question this article is here to answer.

The Dollar’s Quiet Retreat

To understand why central banks are buying gold at these levels, you have to look at what they are selling. Or more precisely — what they are quietly buying less of. The answer is U.S. Treasury securities.

For decades, holding U.S. Treasuries was the safest and most logical thing a central bank could do. They were backed by the most powerful economy in the world, denominated in the world’s reserve currency, and considered to carry virtually no risk of default. But ‘safe’ depends entirely on what you are safe from. And the definition of risk has expanded.

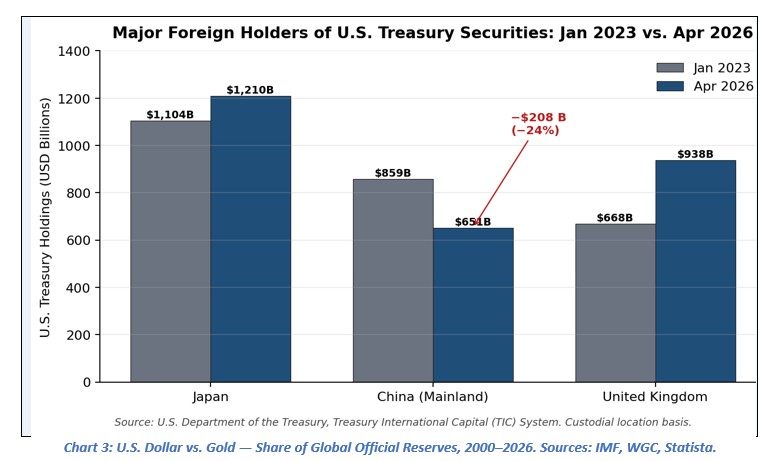

China is the clearest example. At its peak, China held over $1 trillion in U.S. government debt. By January 2023, that number had already fallen to $859 billion. By December 2025, it stood at $683 billion. By April 2026, it had declined further to $651 billion. That is a reduction of more than $400 billion in holdings — a deliberate, sustained, and unmistakable shift in how China stores its national wealth.

Meanwhile, the International Monetary Fund’s own COFER database — which tracks the currency composition of global reserve assets — shows the dollar’s share of allocated reserves dropping to 56.32% in Q2 of 2025. The IMF noted, correctly, that much of this quarterly move was due to the dollar’s depreciation against other currencies, which mechanically inflated the value of non-dollar holdings. But even after stripping out those valuation effects, the long-term downward trend persists. Active diversification — real portfolio decisions by real people — is happening.

In 2026, a milestone was reached that would have seemed unimaginable just years ago. For the first time since 1996, gold overtook U.S. Treasury securities as a share of global central bank reserves. Gold reached roughly 27% of total official reserves, compared to 22% for U.S. debt. The asset that the modern financial system was designed to marginalize — gold — is now more prominent in the vaults of the world’s monetary institutions than the bonds of the world’s largest economy.

Table 2: Foreign Holdings of U.S. Treasury Securities — Key Actors (USD Billions)

| Country | Jan 2023 ($B) | Dec 2025 ($B) | Apr 2026 ($B) | Trend |

| Japan | $1,104.4 | $1,185.5 | $1,209.9 | ↑ Increase |

| China (Mainland) | $859.4 | $683.5 | $651.1 | ↓ Significant Decrease |

| United Kingdom | $668.3 | N/A | $937.5 | ↑ Increase (Volatile) |

Source: U.S. Department of the Treasury, Treasury International Capital (TIC) System. Note: TIC data is based on custodial location; ultimate beneficial ownership may differ.

|

Chart 2: China’s U.S. Treasury Holdings vs. Gold Reserves, 2013–2026. Sources: U.S. Treasury, World Gold Council.

The Event That Accelerated Everything

When historians write about the turning point in the global monetary order, they will almost certainly mark February 2022 as the date that changed everything. That was when Western nations, following Russia’s invasion of Ukraine, froze approximately $300 billion of the Russian central bank’s foreign currency reserves. The assets were held abroad. They were denominated in dollars, euros, and pounds. And overnight, they became inaccessible.

Think about what that means for every other central bank watching. A G20 nation — however one judges its actions — had its sovereign reserves effectively confiscated through the financial system. The message was unmistakable: holding reserves in foreign currencies, custodied in foreign financial centers, is not purely an economic decision. It is a geopolitical one. Your reserves can be used as a weapon against you.

This was the single most powerful accelerant to gold buying in modern central banking history. Gold held domestically has no counterparty. It cannot be frozen by a foreign government. It cannot be ‘sanctioned.’ It does not depend on a SWIFT message to move. It is simply there. Research confirms that countries with lower geopolitical alignment with the United States have been among the most aggressive gold buyers since 2022 — and they have been explicit about why.

The logic is not ideological. It is prudential. It is the same logic that makes a homeowner buy a fire extinguisher even if they have never had a fire. You buy it because, if the moment ever comes, you want to be prepared. For dozens of central banks around the world, gold has become that fire extinguisher.

Building the Exit: mBridge, BRICS, and What Comes Next

Buying gold is a defensive move — a way to protect what you already have. But several of the world’s largest economies are also building something new: a financial infrastructure that does not depend on the dollar at all.

The most advanced example is Project mBridge. This is a real, operational platform developed collaboratively by the Bank for International Settlements, the Hong Kong Monetary Authority, the UAE Central Bank, the People’s Bank of China, and — critically — the Saudi Central Bank, which joined in 2024. mBridge uses distributed ledger technology to allow real-time, direct cross-border payments between central banks, entirely bypassing the dollar-based correspondent banking network. In mid-2024, the project reached its ‘minimum viable product’ stage and has since executed real transactions with real value.

The inclusion of Saudi Arabia is not a footnote. It is a seismic signal. Saudi Arabia is the world’s largest oil exporter. For five decades, oil was priced and settled almost exclusively in dollars, creating the ‘petrodollar’ system that recycled energy revenues back into U.S. Treasury demand. When Riyadh joins a platform explicitly designed to facilitate non-dollar settlement — and when major energy producers increasingly accept payment in Chinese renminbi — something structural is shifting in that arrangement.

(Readers interested in how commodity spreads respond to this kind of geopolitical realignment may find it useful to revisit the analysis on arzualvan.com from March 7, 2026, which modeled gold, silver, and oil spread behavior under Middle East conflict scenarios.)

The BRICS nations — Brazil, Russia, India, China, and South Africa, with a growing list of new members — have made de-dollarization a formal political objective. Progress has been uneven, but the direction is clear. Bilateral agreements to settle trade in local currencies are proliferating. Mechanisms like the BRICS Contingent Reserve Arrangement provide a safety net that does not require an IMF bailout denominated in dollars. Even the Pan-African Payment and Settlement System (PAPSS) is quietly building local-currency settlement infrastructure across a continent that the dollar system often treated as a frontier to be accessed, not a partner to be respected.

None of this means the dollar is dying tomorrow. It remains the dominant reserve currency. Its network effects are enormous. But the trend is clear: the world is building the exits, and central banks are buying the asset that works regardless of which door you use.

This Has Happened Before

History is patient. It has seen this story before. After World War II, the world agreed to anchor the international monetary system to the U.S. dollar, which was itself pegged to gold at $35 per ounce. This was the Bretton Woods system, and it worked — until it didn’t. The United States ran persistent deficits to supply the world with dollars, and eventually the world held far more dollar claims than the U.S. had gold to back them. On August 15, 1971, President Nixon closed the gold window. The dollar was no longer convertible to gold. The era of the pure fiat reserve currency had begun.

What happened next is instructive. Even after the formal link to gold was severed, central banks did not abandon it. IMF research has noted wryly that ‘old habits die hard.’ Institutions with long institutional memory — especially in Europe — continued to hold gold, understanding that it was the ultimate backstop of sovereign credibility that no purely fiat system could fully replace.

The second precedent is closer in time. After the 2008 global financial crisis — which originated in U.S. financial markets and spread globally — emerging market central banks began a new wave of reserve diversification. For the first time in decades, central banks became net buyers of gold, reversing a long era of institutional selling. The logic was the same then as now: when the asset at the center of the system generates a crisis, prudent managers look for something that sits outside the system.

The current phase is not a copy of either of those episodes. It is an acceleration. The 2008 impulse to diversify was tactical. The post-2022 impulse is strategic. Central banks are not hedging against a crisis. They are repositioning for a new world order in which monetary power is more distributed, and where no single nation’s domestic policy can hold the entire globe hostage.

|

Chart 3: U.S. Dollar vs. Gold — Share of Global Official Reserves, 2000–2026. Sources: IMF, WGC, Statista.

Table 3: Key Milestones in Global Central Bank Reserve Sentiment (2025–2026)

| Indicator | 2025 Survey (73 respondents) | 2026 Survey (76 respondents) |

| Central banks expecting USD share to decline | 73% | Not separately broken out; trend reinforced |

| CB institutions planning to increase gold | 43% (record) | 45% (new record) |

| CBs expecting global gold reserves to rise | 95% | 83% expect gold share higher in 5 yrs |

| CBs actively managing gold (swaps, leases) | 44% | Rising trend |

| Top reason for holding gold: Crisis protection | ✓ Cited | 90% cited |

| Top reason: Long-term store of value | ✓ Cited | 84% cited |

| Top reason: Portfolio diversification | ✓ Cited | 82% cited |

Source: World Gold Council, Central Bank Gold Reserves Surveys 2025 and 2026.

What the Gold Price Is Telling You

In 2025, gold set 53 new all-time price records. Its average annual price was $3,431 per ounce. This is not just a story about inflation or a weakening dollar, though both played a role. It is a story about what markets do when they sense structural change.

On the COMEX exchange in New York — the world’s largest gold futures market — something unusual was happening. Historically, fewer than 1% of open futures contracts ever led to actual physical delivery. The market was a financial game, disconnected from the vault. But in 2025, delivery rates spiked to around 7% of open interest. Large institutional players — whoever they were — were using the futures market not to bet on the price, but to take physical possession of the metal.

This matters because it tells you something about confidence. When sophisticated buyers decide they want the metal itself, not just a paper claim on it, they are making a statement about counterparty risk, about trust in financial intermediaries, and about what they think the future looks like. The central banks are not alone in this conviction. The physical gold market is tightening, and the price is reflecting a world in which sovereign and institutional demand for a genuinely neutral asset is growing faster than the supply of it.

A Verdict, Not a Forecast

Let me be clear about what this article is and is not saying. This is not a prediction that the dollar will collapse next year. It is not a recommendation to buy gold. It is not a political argument. It is an analysis of what the world’s most careful, most conservative financial institutions are actually doing with their nations’ money.

And what they are doing is this: they are systematically reducing their exposure to a system that once offered safety and now carries geopolitical risk. They are building portfolios that can survive a world where financial sanctions are a weapon of first resort. They are buying an asset with no issuer, no counterparty, and no political address. They are doing it at twice the historical pace, year after year, while simultaneously telling surveyors that they expect the dollar’s role to shrink.

This is not a forecast. It is a verdict. The jury is made up of 73 central banks. They have delivered their conclusion quietly, in the form of gold purchases and survey responses, without press conferences or political speeches. But the signal is unmistakable for anyone paying attention.

Monetary systems do not collapse overnight. Bretton Woods took decades to unravel. The transition we are witnessing now may take another decade or two to complete. But the direction of travel has been set. The foundations of the old order are being quietly replaced — one tonne of gold at a time, one Treasury bond not repurchased, one bilateral trade agreement settled in a local currency rather than dollars.

When the institutions that built the system start building the exits, the thoughtful observer does not look away. They take note. And they think carefully about what it means.

Glossary

Every technical term explained as simply as possible.

Central Bank: A government institution that manages a country’s money supply and foreign reserves. Think of it as the bank that other banks use, and the guardian of a nation’s financial safety.

Reserve Currency: A currency that other countries hold in large quantities because it is widely accepted in international trade. The U.S. dollar is the world’s main reserve currency today.

Foreign Reserves: The savings a country keeps in foreign assets — dollars, gold, bonds — to defend its own currency and pay for international obligations. Like a national emergency fund.

U.S. Treasury Securities (Bonds): Debt issued by the U.S. government. When a country buys a Treasury bond, it is lending money to the United States. It was once considered the safest investment in the world.

Gold Reserves: Physical gold bars held by a central bank, often in its own vaults. Unlike a bond, gold is nobody’s debt. No government can freeze it if it is stored at home.

Petrodollar System: The informal arrangement — established in the 1970s — by which oil was globally priced and paid for in U.S. dollars. This created a constant global demand for dollars, supporting American financial power.

De-dollarization: The process by which countries gradually reduce their reliance on the U.S. dollar for trade, reserves, and financial transactions. Not a sudden event, but a slow structural shift.

Bretton Woods System: The post-World War II agreement that pegged the dollar to gold and other currencies to the dollar. It effectively made the U.S. dollar the world’s reserve currency. It collapsed in 1971.

BRICS: A grouping of major emerging economies — Brazil, Russia, India, China, South Africa, and newer members. They share an interest in reducing dollar dependence and increasing their own influence in global finance.

mBridge (Project mBridge): A technology platform developed by central banks of China, the UAE, Hong Kong, Saudi Arabia, and the BIS that allows countries to make cross-border payments directly, without using U.S. dollar-based banking networks.

CBDC (Central Bank Digital Currency): A digital version of a country’s official currency, issued and controlled by its central bank. Unlike Bitcoin, it is government-backed. mBridge is built on CBDC technology.

IMF COFER: A database maintained by the International Monetary Fund tracking which currencies countries hold in their foreign reserves. It shows whether the world is moving toward or away from dollar dominance.

TIC Data (Treasury International Capital): U.S. government data tracking who holds U.S. Treasury securities globally. It is how we know that China has reduced its Treasury holdings significantly.

Counterparty Risk: The risk that the other party in a financial deal might fail, default, or be prevented from fulfilling their obligation. Gold held domestically has no counterparty. A dollar bond depends entirely on the U.S. government’s goodwill.

Triffin Dilemma: A fundamental conflict in any reserve currency system: the issuing country must run deficits to supply the world with its currency, but those deficits eventually undermine trust in the currency. Named after economist Robert Triffin.

COMEX: The Commodity Exchange, a major U.S. financial market where gold, silver, and other commodities are traded via futures contracts. A futures contract is an agreement to buy or sell at a set price on a future date.

Open Interest: The total number of outstanding futures contracts that have not yet been settled or closed. When COMEX open interest leads to actual physical gold delivery, it signals real, not speculative, demand.

Multipolar Monetary Order: A global financial system in which no single currency or country dominates. Power is spread across several major currencies, trading blocs, and payment systems.

Sanctions (Financial): Measures by which one country or group of countries restricts access to the financial system for another country or entity. In 2022, the West froze Russian central bank reserves — an unprecedented use of financial sanctions against a major power.

World Gold Council (WGC): An international organization funded by major gold mining companies that conducts research and promotes gold investment. Its annual surveys and demand data are the most authoritative source on global gold flows.

Sources and References

- World Gold Council. (2025). 2025 Central Bank Gold Reserves Survey. gold.org/goldhub/research/central-bank-gold-reserves-survey-2025

- World Gold Council. (2026, January). Gold Demand Trends Full Year 2025 — Central Banks. gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-full-year-2025/central-banks

- World Gold Council. (2026, January). Gold Demand Trends Full Year 2025 — Overview. gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-full-year-2025

- Informed Clearly. (2026). Record Central Bank Gold Reserves: WGC 2026. informedclearly.com/en/economy/55699

- World Gold Council. (2026). Central Banks Set to Step Up Gold Buying Over Next Year [Press Release]. gold.org/news-and-events/press-releases/central-banks-set-step-gold-buying-over-next-year

- Equiti. (2026). Central Bank Gold Buying Cooled in 2025, But Stayed Far Above Historical Norms. equiti.com

- OnlineGold.org. (2026). Central Bank Gold Reserves 2026. onlinegold.org/analysis/central-bank-gold-reserves-2026

- U.S. Department of the Treasury. TIC Data: Historical Major Foreign Holders. ticdata.treasury.gov/Publish/mfhhis01.txt

- U.S. Department of the Treasury. TIC Data: Major Foreign Holders of Treasury Securities (Monthly). ticdata.treasury.gov

- International Monetary Fund. (2025, October 1). COFER Q2 2025 Data Release. data.imf.org

- IMF Blog. (2025, October 1). Dollar’s Share of Reserves Held Steady in Second Quarter When Adjusted for FX Moves. imf.org/en/blogs/articles/2025/10/01

- IMF Blog. (2024, June 11). Dollar Dominance in the International Reserve System: An Update. imf.org/en/blogs/articles/2024/06/11

- Brookings Institution. How Important Are Central Bank Holdings of Gold? brookings.edu/articles/how-important-are-central-bank-holdings-of-gold

- Bank for International Settlements. (2024, June 5). Project mBridge Reaches Minimum Viable Product Stage. bis.org/press/p240605.htm

- Bank for International Settlements. Project mBridge: Connecting Economies Through CBDCs. bis.org/about/bisih/topics/cbdc/mcbdc_bridge.htm

- European Central Bank. (2025, June). The International Role of the Euro. ecb.europa.eu

- CEPR/VoxEU. The Operation and Demise of the Bretton Woods System: 1958–1971. cepr.org/voxeu/columns

- International Monetary Fund. (2019). Old Habits Die Hard: The Case of the Gold Standard. IMF Working Paper WP/19/161.

- Federal Reserve History. The Smithsonian Agreement. federalreservehistory.org/essays/smithsonian-agreement

- World Gold Council. History of Gold: Bretton Woods System. gold.org/history-gold/bretton-woods-system

- World Gold Council. Gold Market Primer: Market Size and Structure. gold.org/goldhub/research/market-primer

- Seventy-three percent. Hold that number in your mind for a moment. Not a majority of disgruntled economists. Not a fringe of conspiracy theorists. We are talking about 73 of the world’s own central banks — the very institutions that guard their nations’ sovereign wealth, that sit at the apex of global finance, that have spent decades building their reserves in U.S. dollars — and in 2025, nearly three-quarters of them told the World Gold Council the same thing: they expect the dollar’s share of global reserves to fall. Significantly. In the next five years.That is not a market signal. That is not a passing sentiment. It is a verdict. And when the judges are the world’s monetary authorities, every investor, every policymaker, and honestly every thinking person on the planet should pay attention.

So what is happening? Why are the guardians of the world’s reserve system quietly stepping away from the asset that once underpinned it? And what are they buying instead? The answers tell a story about trust, power, and the way money itself is being reinvented.

863 Tonnes. Every Single Year. This Is No Accident.

In 2025, the world’s central banks collectively purchased 863 tonnes of gold. This is confirmed by the World Gold Council’s official data. The number sounds dry until you consider the context: in the decade before 2022, the average annual purchase was around 473 tonnes. Then, starting in 2022, something broke open. Central banks bought over 1,000 tonnes per year, for three consecutive years, shattering every modern record. Even in 2025, when some slowing was expected, the total landed at nearly double the pre-2022 baseline.

Think of it this way. Imagine a family that used to spend €500 a month on groceries. Then something changed at the supermarket — maybe the quality collapsed, maybe the owner started threatening customers — and suddenly they started spending €1,100 a month. A year later, they spend €900. Some analysts say: ‘Look, they’re cutting back.’ But the truth is they are still spending nearly twice what they used to. The new normal is not the old normal. The behavior has permanently changed.

The buyers in 2025 were geographically wide. Poland’s central bank led the field with 102 tonnes — its second consecutive year at the top. Kazakhstan added 57 tonnes, its highest annual purchase since 1993. Brazil re-entered the market after four years away, picking up 43 tonnes. Turkey added 27 tonnes, as did China officially. The Czech Republic quietly added 20 tonnes as part of a steady, multi-year program.

There is also a hidden layer to this story. The World Gold Council estimates that roughly 57% of total central bank demand in 2025 came from buyers who never publicly reported their purchases. These are institutions — widely suspected to include China and others — who accumulate gold through state-owned enterprises or commercial banks to avoid moving the price against their own future purchases. When you account for this unreported buying, some independent estimates put the true 2025 figure closer to 1,237 tonnes. The disclosed number is already striking. The full picture may be even more so.

Table 1: Major Central Bank Gold Purchases, 2025

Country / Institution Reported Purchase (Tonnes) Key Driver Source National Bank of Poland 102 National financial security; second consecutive year as top buyer WGC 2025 National Bank of Kazakhstan 57 Record purchase since 1993; leverages domestic mine output WGC 2025 Central Bank of Brazil 43 Re-entered market after four-year absence (Q3/Q4 purchases) WGC 2025 Central Bank of Turkey 27 Consistent multi-year accumulation program WGC 2025 People’s Bank of China 27 Official reported figure; widely believed to hold additional unreported positions WGC 2025 Czech National Bank 20 Steady ongoing program to increase gold share of reserves WGC 2025 Total (All Reported) 863.3 Net central bank purchases globally, 2025 WGC 2025 Source: World Gold Council, Gold Demand Trends Full Year 2025. Unreported buying estimated at ~57% of total demand.

Chart 1: Net Central Bank Gold Purchases, 2010–2025 (Tonnes). Source: World Gold Council.

The Survey That Changed Everything

Each year, the World Gold Council conducts a survey of the world’s reserve managers. These are the professionals who sit inside central banks and decide how to protect their nation’s wealth. In 2025, a record 73 central banks responded — the highest participation in the survey’s history. What they said was remarkable.

Seventy-three percent of respondents expect the U.S. dollar’s share of global reserves to be lower — moderately or significantly — within five years. Read that sentence again. These are not academics speculating in journals. These are the people who actually manage the world’s reserve assets, day by day, making real decisions that determine what their nations’ wealth looks like a decade from now.

And it is not merely an opinion. Opinion translates into action. A record 43% of those same central banks told the survey they plan to increase their gold holdings in the coming twelve months. Zero said they planned to decrease them. Ninety-five percent expect total global official gold reserves to rise over the next year. These are not passive observers of a trend. They are the trend.

By 2026, the data had grown even more assertive. A follow-up survey — this time with 76 central bank respondents — found 45% planning to add gold, another record. Eighty-three percent said they expect gold’s share of total reserves to be higher in five years. The motivations they cited were consistent and telling: crisis protection (90% of respondents), long-term store of value (84%), and portfolio diversification (82%).

The language of ‘crisis protection’ and ‘store of value’ matters here. These are not reasons to hold an asset when everything is fine. They are reasons to hold an asset when you are not sure everything will remain fine. Read between the lines: the world’s reserve managers are buying insurance. Insurance against what? That is the question this article is here to answer.

The Dollar’s Quiet Retreat

To understand why central banks are buying gold at these levels, you have to look at what they are selling. Or more precisely — what they are quietly buying less of. The answer is U.S. Treasury securities.

For decades, holding U.S. Treasuries was the safest and most logical thing a central bank could do. They were backed by the most powerful economy in the world, denominated in the world’s reserve currency, and considered to carry virtually no risk of default. But ‘safe’ depends entirely on what you are safe from. And the definition of risk has expanded.

China is the clearest example. At its peak, China held over $1 trillion in U.S. government debt. By January 2023, that number had already fallen to $859 billion. By December 2025, it stood at $683 billion. By April 2026, it had declined further to $651 billion. That is a reduction of more than $400 billion in holdings — a deliberate, sustained, and unmistakable shift in how China stores its national wealth.

Meanwhile, the International Monetary Fund’s own COFER database — which tracks the currency composition of global reserve assets — shows the dollar’s share of allocated reserves dropping to 56.32% in Q2 of 2025. The IMF noted, correctly, that much of this quarterly move was due to the dollar’s depreciation against other currencies, which mechanically inflated the value of non-dollar holdings. But even after stripping out those valuation effects, the long-term downward trend persists. Active diversification — real portfolio decisions by real people — is happening.

In 2026, a milestone was reached that would have seemed unimaginable just years ago. For the first time since 1996, gold overtook U.S. Treasury securities as a share of global central bank reserves. Gold reached roughly 27% of total official reserves, compared to 22% for U.S. debt. The asset that the modern financial system was designed to marginalize — gold — is now more prominent in the vaults of the world’s monetary institutions than the bonds of the world’s largest economy.

Table 2: Foreign Holdings of U.S. Treasury Securities — Key Actors (USD Billions)

Country Jan 2023 ($B) Dec 2025 ($B) Apr 2026 ($B) Trend Japan $1,104.4 $1,185.5 $1,209.9 ↑ Increase China (Mainland) $859.4 $683.5 $651.1 ↓ Significant Decrease United Kingdom $668.3 N/A $937.5 ↑ Increase (Volatile) Source: U.S. Department of the Treasury, Treasury International Capital (TIC) System. Note: TIC data is based on custodial location; ultimate beneficial ownership may differ.

Chart 2: China’s U.S. Treasury Holdings vs. Gold Reserves, 2013–2026. Sources: U.S. Treasury, World Gold Council.

The Event That Accelerated Everything

When historians write about the turning point in the global monetary order, they will almost certainly mark February 2022 as the date that changed everything. That was when Western nations, following Russia’s invasion of Ukraine, froze approximately $300 billion of the Russian central bank’s foreign currency reserves. The assets were held abroad. They were denominated in dollars, euros, and pounds. And overnight, they became inaccessible.

Think about what that means for every other central bank watching. A G20 nation — however one judges its actions — had its sovereign reserves effectively confiscated through the financial system. The message was unmistakable: holding reserves in foreign currencies, custodied in foreign financial centers, is not purely an economic decision. It is a geopolitical one. Your reserves can be used as a weapon against you.

This was the single most powerful accelerant to gold buying in modern central banking history. Gold held domestically has no counterparty. It cannot be frozen by a foreign government. It cannot be ‘sanctioned.’ It does not depend on a SWIFT message to move. It is simply there. Research confirms that countries with lower geopolitical alignment with the United States have been among the most aggressive gold buyers since 2022 — and they have been explicit about why.

The logic is not ideological. It is prudential. It is the same logic that makes a homeowner buy a fire extinguisher even if they have never had a fire. You buy it because, if the moment ever comes, you want to be prepared. For dozens of central banks around the world, gold has become that fire extinguisher.

Building the Exit: mBridge, BRICS, and What Comes Next

Buying gold is a defensive move — a way to protect what you already have. But several of the world’s largest economies are also building something new: a financial infrastructure that does not depend on the dollar at all.

The most advanced example is Project mBridge. This is a real, operational platform developed collaboratively by the Bank for International Settlements, the Hong Kong Monetary Authority, the UAE Central Bank, the People’s Bank of China, and — critically — the Saudi Central Bank, which joined in 2024. mBridge uses distributed ledger technology to allow real-time, direct cross-border payments between central banks, entirely bypassing the dollar-based correspondent banking network. In mid-2024, the project reached its ‘minimum viable product’ stage and has since executed real transactions with real value.

The inclusion of Saudi Arabia is not a footnote. It is a seismic signal. Saudi Arabia is the world’s largest oil exporter. For five decades, oil was priced and settled almost exclusively in dollars, creating the ‘petrodollar’ system that recycled energy revenues back into U.S. Treasury demand. When Riyadh joins a platform explicitly designed to facilitate non-dollar settlement — and when major energy producers increasingly accept payment in Chinese renminbi — something structural is shifting in that arrangement.

(Readers interested in how commodity spreads respond to this kind of geopolitical realignment may find it useful to revisit the analysis on arzualvan.com from March 7, 2026, which modeled gold, silver, and oil spread behavior under Middle East conflict scenarios.)

The BRICS nations — Brazil, Russia, India, China, and South Africa, with a growing list of new members — have made de-dollarization a formal political objective. Progress has been uneven, but the direction is clear. Bilateral agreements to settle trade in local currencies are proliferating. Mechanisms like the BRICS Contingent Reserve Arrangement provide a safety net that does not require an IMF bailout denominated in dollars. Even the Pan-African Payment and Settlement System (PAPSS) is quietly building local-currency settlement infrastructure across a continent that the dollar system often treated as a frontier to be accessed, not a partner to be respected.

None of this means the dollar is dying tomorrow. It remains the dominant reserve currency. Its network effects are enormous. But the trend is clear: the world is building the exits, and central banks are buying the asset that works regardless of which door you use.

This Has Happened Before

History is patient. It has seen this story before. After World War II, the world agreed to anchor the international monetary system to the U.S. dollar, which was itself pegged to gold at $35 per ounce. This was the Bretton Woods system, and it worked — until it didn’t. The United States ran persistent deficits to supply the world with dollars, and eventually the world held far more dollar claims than the U.S. had gold to back them. On August 15, 1971, President Nixon closed the gold window. The dollar was no longer convertible to gold. The era of the pure fiat reserve currency had begun.

What happened next is instructive. Even after the formal link to gold was severed, central banks did not abandon it. IMF research has noted wryly that ‘old habits die hard.’ Institutions with long institutional memory — especially in Europe — continued to hold gold, understanding that it was the ultimate backstop of sovereign credibility that no purely fiat system could fully replace.

The second precedent is closer in time. After the 2008 global financial crisis — which originated in U.S. financial markets and spread globally — emerging market central banks began a new wave of reserve diversification. For the first time in decades, central banks became net buyers of gold, reversing a long era of institutional selling. The logic was the same then as now: when the asset at the center of the system generates a crisis, prudent managers look for something that sits outside the system.

The current phase is not a copy of either of those episodes. It is an acceleration. The 2008 impulse to diversify was tactical. The post-2022 impulse is strategic. Central banks are not hedging against a crisis. They are repositioning for a new world order in which monetary power is more distributed, and where no single nation’s domestic policy can hold the entire globe hostage.

Chart 3: U.S. Dollar vs. Gold — Share of Global Official Reserves, 2000–2026. Sources: IMF, WGC, Statista.

Table 3: Key Milestones in Global Central Bank Reserve Sentiment (2025–2026)

Indicator 2025 Survey (73 respondents) 2026 Survey (76 respondents) Central banks expecting USD share to decline 73% Not separately broken out; trend reinforced CB institutions planning to increase gold 43% (record) 45% (new record) CBs expecting global gold reserves to rise 95% 83% expect gold share higher in 5 yrs CBs actively managing gold (swaps, leases) 44% Rising trend Top reason for holding gold: Crisis protection ✓ Cited 90% cited Top reason: Long-term store of value ✓ Cited 84% cited Top reason: Portfolio diversification ✓ Cited 82% cited Source: World Gold Council, Central Bank Gold Reserves Surveys 2025 and 2026.

What the Gold Price Is Telling You

In 2025, gold set 53 new all-time price records. Its average annual price was $3,431 per ounce. This is not just a story about inflation or a weakening dollar, though both played a role. It is a story about what markets do when they sense structural change.

On the COMEX exchange in New York — the world’s largest gold futures market — something unusual was happening. Historically, fewer than 1% of open futures contracts ever led to actual physical delivery. The market was a financial game, disconnected from the vault. But in 2025, delivery rates spiked to around 7% of open interest. Large institutional players — whoever they were — were using the futures market not to bet on the price, but to take physical possession of the metal.

This matters because it tells you something about confidence. When sophisticated buyers decide they want the metal itself, not just a paper claim on it, they are making a statement about counterparty risk, about trust in financial intermediaries, and about what they think the future looks like. The central banks are not alone in this conviction. The physical gold market is tightening, and the price is reflecting a world in which sovereign and institutional demand for a genuinely neutral asset is growing faster than the supply of it.

A Verdict, Not a Forecast

Let me be clear about what this article is and is not saying. This is not a prediction that the dollar will collapse next year. It is not a recommendation to buy gold. It is not a political argument. It is an analysis of what the world’s most careful, most conservative financial institutions are actually doing with their nations’ money.

And what they are doing is this: they are systematically reducing their exposure to a system that once offered safety and now carries geopolitical risk. They are building portfolios that can survive a world where financial sanctions are a weapon of first resort. They are buying an asset with no issuer, no counterparty, and no political address. They are doing it at twice the historical pace, year after year, while simultaneously telling surveyors that they expect the dollar’s role to shrink.

This is not a forecast. It is a verdict. The jury is made up of 73 central banks. They have delivered their conclusion quietly, in the form of gold purchases and survey responses, without press conferences or political speeches. But the signal is unmistakable for anyone paying attention.

Monetary systems do not collapse overnight. Bretton Woods took decades to unravel. The transition we are witnessing now may take another decade or two to complete. But the direction of travel has been set. The foundations of the old order are being quietly replaced — one tonne of gold at a time, one Treasury bond not repurchased, one bilateral trade agreement settled in a local currency rather than dollars.

When the institutions that built the system start building the exits, the thoughtful observer does not look away. They take note. And they think carefully about what it means.

Glossary

Every technical term explained as simply as possible.

Central Bank: A government institution that manages a country’s money supply and foreign reserves. Think of it as the bank that other banks use, and the guardian of a nation’s financial safety.

Reserve Currency: A currency that other countries hold in large quantities because it is widely accepted in international trade. The U.S. dollar is the world’s main reserve currency today.

Foreign Reserves: The savings a country keeps in foreign assets — dollars, gold, bonds — to defend its own currency and pay for international obligations. Like a national emergency fund.

U.S. Treasury Securities (Bonds): Debt issued by the U.S. government. When a country buys a Treasury bond, it is lending money to the United States. It was once considered the safest investment in the world.

Gold Reserves: Physical gold bars held by a central bank, often in its own vaults. Unlike a bond, gold is nobody’s debt. No government can freeze it if it is stored at home.

Petrodollar System: The informal arrangement — established in the 1970s — by which oil was globally priced and paid for in U.S. dollars. This created a constant global demand for dollars, supporting American financial power.

De-dollarization: The process by which countries gradually reduce their reliance on the U.S. dollar for trade, reserves, and financial transactions. Not a sudden event, but a slow structural shift.

Bretton Woods System: The post-World War II agreement that pegged the dollar to gold and other currencies to the dollar. It effectively made the U.S. dollar the world’s reserve currency. It collapsed in 1971.

BRICS: A grouping of major emerging economies — Brazil, Russia, India, China, South Africa, and newer members. They share an interest in reducing dollar dependence and increasing their own influence in global finance.

mBridge (Project mBridge): A technology platform developed by central banks of China, the UAE, Hong Kong, Saudi Arabia, and the BIS that allows countries to make cross-border payments directly, without using U.S. dollar-based banking networks.

CBDC (Central Bank Digital Currency): A digital version of a country’s official currency, issued and controlled by its central bank. Unlike Bitcoin, it is government-backed. mBridge is built on CBDC technology.

IMF COFER: A database maintained by the International Monetary Fund tracking which currencies countries hold in their foreign reserves. It shows whether the world is moving toward or away from dollar dominance.

TIC Data (Treasury International Capital): U.S. government data tracking who holds U.S. Treasury securities globally. It is how we know that China has reduced its Treasury holdings significantly.

Counterparty Risk: The risk that the other party in a financial deal might fail, default, or be prevented from fulfilling their obligation. Gold held domestically has no counterparty. A dollar bond depends entirely on the U.S. government’s goodwill.

Triffin Dilemma: A fundamental conflict in any reserve currency system: the issuing country must run deficits to supply the world with its currency, but those deficits eventually undermine trust in the currency. Named after economist Robert Triffin.

COMEX: The Commodity Exchange, a major U.S. financial market where gold, silver, and other commodities are traded via futures contracts. A futures contract is an agreement to buy or sell at a set price on a future date.

Open Interest: The total number of outstanding futures contracts that have not yet been settled or closed. When COMEX open interest leads to actual physical gold delivery, it signals real, not speculative, demand.

Multipolar Monetary Order: A global financial system in which no single currency or country dominates. Power is spread across several major currencies, trading blocs, and payment systems.

Sanctions (Financial): Measures by which one country or group of countries restricts access to the financial system for another country or entity. In 2022, the West froze Russian central bank reserves — an unprecedented use of financial sanctions against a major power.

World Gold Council (WGC): An international organization funded by major gold mining companies that conducts research and promotes gold investment. Its annual surveys and demand data are the most authoritative source on global gold flows.

Sources and References

- World Gold Council. (2025). 2025 Central Bank Gold Reserves Survey. gold.org/goldhub/research/central-bank-gold-reserves-survey-2025

- World Gold Council. (2026, January). Gold Demand Trends Full Year 2025 — Central Banks. gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-full-year-2025/central-banks

- World Gold Council. (2026, January). Gold Demand Trends Full Year 2025 — Overview. gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-full-year-2025

- Informed Clearly. (2026). Record Central Bank Gold Reserves: WGC 2026. informedclearly.com/en/economy/55699

- World Gold Council. (2026). Central Banks Set to Step Up Gold Buying Over Next Year [Press Release]. gold.org/news-and-events/press-releases/central-banks-set-step-gold-buying-over-next-year

- Equiti. (2026). Central Bank Gold Buying Cooled in 2025, But Stayed Far Above Historical Norms. equiti.com

- OnlineGold.org. (2026). Central Bank Gold Reserves 2026. onlinegold.org/analysis/central-bank-gold-reserves-2026

- U.S. Department of the Treasury. TIC Data: Historical Major Foreign Holders. ticdata.treasury.gov/Publish/mfhhis01.txt

- U.S. Department of the Treasury. TIC Data: Major Foreign Holders of Treasury Securities (Monthly). ticdata.treasury.gov

- International Monetary Fund. (2025, October 1). COFER Q2 2025 Data Release. data.imf.org

- IMF Blog. (2025, October 1). Dollar’s Share of Reserves Held Steady in Second Quarter When Adjusted for FX Moves. imf.org/en/blogs/articles/2025/10/01

- IMF Blog. (2024, June 11). Dollar Dominance in the International Reserve System: An Update. imf.org/en/blogs/articles/2024/06/11

- Brookings Institution. How Important Are Central Bank Holdings of Gold? brookings.edu/articles/how-important-are-central-bank-holdings-of-gold

- Bank for International Settlements. (2024, June 5). Project mBridge Reaches Minimum Viable Product Stage. bis.org/press/p240605.htm

- Bank for International Settlements. Project mBridge: Connecting Economies Through CBDCs. bis.org/about/bisih/topics/cbdc/mcbdc_bridge.htm

- European Central Bank. (2025, June). The International Role of the Euro. ecb.europa.eu

- CEPR/VoxEU. The Operation and Demise of the Bretton Woods System: 1958–1971. cepr.org/voxeu/columns

- International Monetary Fund. (2019). Old Habits Die Hard: The Case of the Gold Standard. IMF Working Paper WP/19/161.

- Federal Reserve History. The Smithsonian Agreement. federalreservehistory.org/essays/smithsonian-agreement

- World Gold Council. History of Gold: Bretton Woods System. gold.org/history-gold/bretton-woods-system

- World Gold Council. Gold Market Primer: Market Size and Structure. gold.org/goldhub/research/market-primer

- The Golden Speculator / Jinlow Substack. (2025, December). December 2025 COMEX Delivery Data. jinlow.substack.com

- World Gold Council. (2025). Gold Demand Trends Full Year 2024 — Central Banks. gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-full-year-2024/central-banks

- Bank for International Settlements. (2025). Counterparty Risk, Collateral and Central Bank Operations. BIS Quarterly Review, June 2025.

- Statista / Visual Capitalist. (2026). Share of Gold and U.S. Debt Holdings in Foreign Central Banks’ Reserves. statista.com/chart/35763

- Bank for International Settlements. (2008). FX Reserve Management: Elements and Evolution. BIS Paper No. 38.

Arzu Alvan. (2026, March 7). Gold, Silver, and Oil Spread Behavior Under Middle East Conflict Scenarios. arzualvan.com

The Golden Speculator / Jinlow Substack. (2025, December). December 2025 COMEX Delivery Data. jinlow.substack.com

- World Gold Council. (2025). Gold Demand Trends Full Year 2024 — Central Banks. gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-full-year-2024/central-banks

- Bank for International Settlements. (2025). Counterparty Risk, Collateral and Central Bank Operations. BIS Quarterly Review, June 2025.

- Statista / Visual Capitalist. (2026). Share of Gold and U.S. Debt Holdings in Foreign Central Banks’ Reserves. statista.com/chart/35763

- Bank for International Settlements. (2008). FX Reserve Management: Elements and Evolution. BIS Paper No. 38.

Bozdereli, A.A. (2026, March 7). Gold, Silver, and Oil Spread Behavior Under Middle East Conflict Scenarios. arzualvan.com